Required minimum distributions (RMD) are just that, minimum amounts of money you need to withdraw from your retirement account once you reach a certain age. At the time of this writing, you’ll generally need to take RMDs from your traditional IRA the year you turn 72 years old.

This article explores how to track your RMDs in Banktivity.

Let’s assume that for this example you have one retirement account, a traditional IRA and a checking account. The IRA is the account from which you’ll need to make withdrawal (or distribute) money and it will go into your checking account. Your brokerage account will also withhold some taxes so this article covers how to track that as well.

For most people this happens by selling stock, mutual funds or other security in your IRA and then transferring the proceeds to your checking. In Banktivity this is best captured with two different transactions:

- The sale of the security asset in your IRA account

- A split transfer of the net proceeds into your checking account, less the amount withheld for taxes

Here is a transaction in the IRA account selling 50 shares of Apple for a gross amount of $7,500.

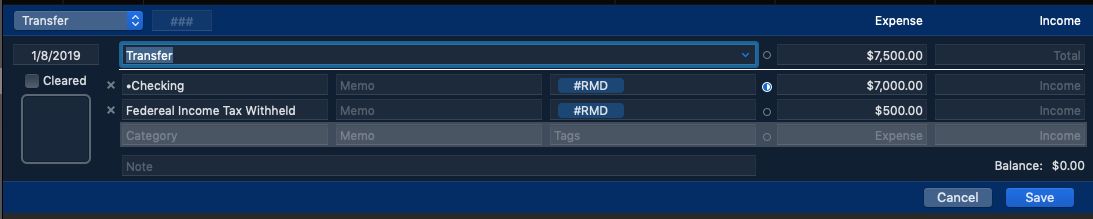

Now immediately after that transaction, we have the split transfer. This transaction moves the $7,500 from your IRA, takes out $500 for taxes and puts the remaining $7,000 into your Checking.

Note on Tags

Tags in Banktivity allow you to analyze transactions across categories and transfers. They are denoted in Banktivity with #<name>. Astute readers will also notice the “#RMD” tags in the screenshot above. By tagging both of the split items in the transaction it allows you to later analyze all transactions related to required minimum distributions. This also allows you to report on RMDs across multiple IRA accounts or other retirement accounts.