How I found myself in debt is a pretty common story for many. In fact it happened, almost unconsciously, while chasing The American Dream. I found a decent paying job, bought a house, went to college and started raising a family. After some years of climbing the corporate ladder, I realized that I was not fulfilled, so I joined my wife’s internet services company. Things were good, and I felt successful. All the boxes we’re checked, except one: my debt.

Over the years carrying student loan debt, a mortgage and credit cards all seemed perfectly normal. I didn’t think about it much, and I never worried. Then something happened, an unexpected job opportunity opened with IGG Software. I plugged my numbers into their app, Banktivity. And there it was, a negative net worth! What? Is that even possible!? (And yes, of course, it is possible for all of us starting out with home, auto and student loans, but it is just a bummer when you actually see it.)

I wanted to share my story because it’s real and it’s working. My debt is rapidly shrinking. But I’m not here to echo another, “use this system to get out of debt,” so much as to show you how I took several disciplines and put them together in my own “personalized” approach. Not only does this work for me, but is something I’m really excited about. After all it’s personal finance, which means it absolutely has to work for your own situation.

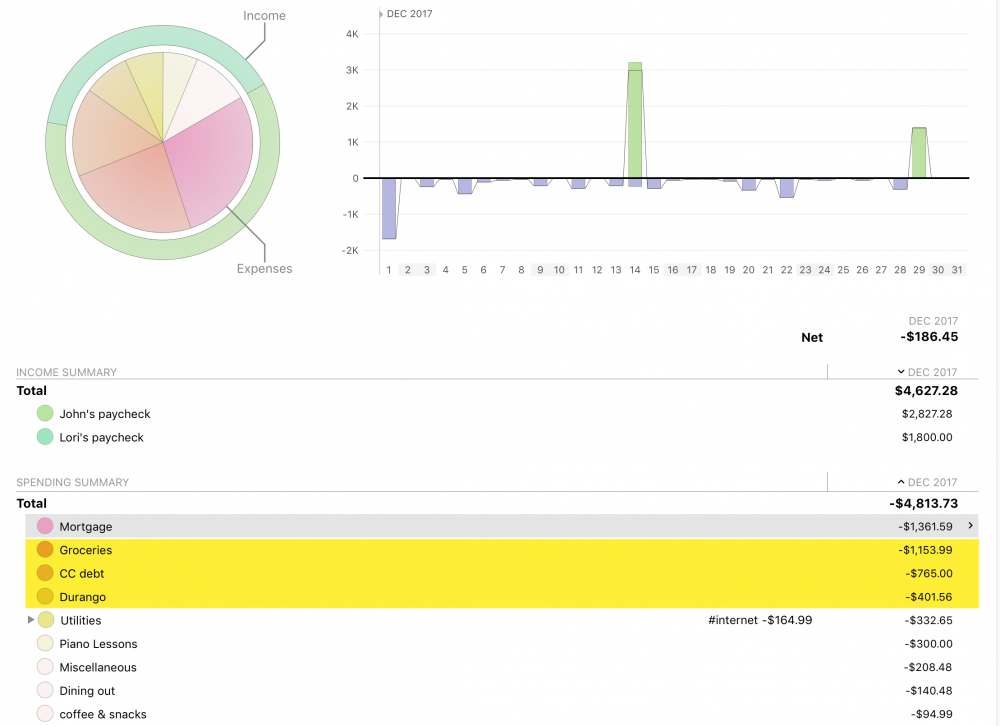

I’m an analyst by nature and always fond of saying, “a data-driven picture is better than a 1,000 words.”

So lets jump right in. Over the years here at IGG, I’ve learned the core principles of personal finance management through learning the features and tools of Banktivity. It might sound obvious, but getting started with the basics was essential. Making the step from simply tracking all of my financial transactions to categorizing them gave me new insights into how we’re spending our money.

However, tracking alone wasn’t helping. Month after month things really just didn’t seem to be changing for the better because, well, they weren’t.

I was simply watching my financial habits, not changing them. Ouch! Spending more than we make was unsustainable. Time to tackle that debt and reign in unnecessary spending!

That’s when it hit me, I am the proverbial example of insanity, repeating the same actions while expecting different results! I knew I had to up my game, take the basics I’ve learned and put a strategy in place that would deliver the results I so desperately needed to see.

The first thing I did was think about the different methods for paying off debt. I’ve come across many different approaches over the years and the one that stood out for me the most was the “Debt Snowball Method” (as promised no specific methods today, but you can get all the details on the debt snowball method here). In a nutshell, the idea is you sort your debt based on amount owed, and start by tackling the smallest debt first. Using Banktivity, I looked at all of my credit cards, loans and other debts and arranged them from smallest to largest. Then something popped out at me:

If I tackled my auto loan first, my debt snowball would double in size, and roll over to the next couple of credit cards in no time!

It’s one of my largest monthly payments, but the loan was close to maturity, only about 10 months to go. Getting this debt wiped out didn’t feel too far fetched.

While the debt-snowball method says start with the lowest principal first, I liked the idea of kick starting my debt reduction by wiping out the car payment. I also looked at my payment pattern with my credit cards. For years I’ve made sure that every month, I pay as much as I can over the minimum. Combined, this was about $400 over the minimum spread over all the credit card payments. So I essentially had $400 a month extra that I was putting toward credit card payments. My monthly car payment is also about $400. So if I took a break from paying the extra on the credit cards, I could essentially double up the payment toward the car loan and get it paid off in a few months.

This deviates from the pure principle of the debt snowball, but it made the most sense for my situation. Knocking off the lowest balance credit card first would have been faster, but the net gain to my snowball would have been much lower, only about $40 vs $400!

I started a few months back and next month the Durango will be paid off! Seeing the loan principal drop so fast is super inspiring. I could see the difference right away. Prior to taking on this strategy the needle seemed to barely move on any of my debts. Now I am seeing significant drops month after month.

Next up, my Home Depot card. With this size of a snowball, I’ll pay it off in 2 months. Then my Discover card following that! As the balances to tackle get a little larger, so does my snowball! What makes this all so brilliant, is the psychological factor. It is a huge relief seeing these debts finally starting to disappear. It’s infectious once you start.

Now the snowball is rolling, what next?

We didn’t stop there! At the same time, my wife undertook the assignment of moving our larger credit card balances to new zero percent cards. So even though we are only paying the minimum amount on those cards, those minimum payments are actually bringing down principal balances instead of mostly interest. Not bad, right?

So after just several months following the debt snowball method, we will have paid off our car loan 5 months early and doubled our snowball’s momentum to the point where the next credit card will be crushed in 2 months. And another surprise, both mine and my wife’s credit scores jumped up over 30 points! Most of all, we see light at the end of the tunnel! After years of due diligence of paying our debt at a snails pace, I can’t tell you how awesome it is to see these accounts actually being paid off. I’m even excited to pay my bills now! 2018 is looking better than ever!

So this is my story of how I personalized the debt snowball method to work for me. I hope there was something in it that helps you and your family’s financial journey. If you have your own personal finance story we’d love to hear about it! Leave a comment below or find us on Twitter, Facebook or Reddit. If you have a longer personal finance success story to tell, don’t be shy, email us at media at iggsoftware.com, we might even work with you on publishing it here to inspire more people.

Here’s to an awesome 2018!

Thank you! I’m going to look into this more because I would definitely like to see my debt drop.

I did a snowball over 20 years ago, still debt free. However I found that personal values are as, if not more important to sucess than one size fits all answer. I listed my debt to balance outstanding, monthly interest charges, and minimum payment payoff. Some times doing a higher balance with higher interest gives an emotional boast that becomes important to keep your process going. Its important to understand the theroy but the application becomes much more personal.

Great advice! Im fortunate to have zero debt at this stage of my life and this would have been a valuable lesson to apply earlier in my life. Now I have a great Third-party article that I could pass on to those in need.

What are zero percent cards, and how do you get one?

Hi Jim, 0 percent cards are really a temporary offer from an existing credit card you have, usually 12 months where you can move debt to no interest (if you have the available credit open). There is a minimum fee for the transfer, but the great thing is you’ll have the 12 months or more to pay down principal instead of interest, as each payment pays down 100% principal. In my experience the fees have always been worth it.

One tip, set a calendar reminder for the month before your promotional period expires, so you can survey current offers, and transfer the balance again if it’s worth it.

This system does work as my husband and I tackled our huge debt after we were married using this method. Combining our separate credit cards and 2 car loans and a student loan was enough to pay for a make believe BMW that we didn’t drive! After 3 years, we were debt free. That was 7 years ago. But as time wore on, we again have 2 car payments (1 loan 1 lease) and a mild credit card floating debt. My salary has increased and my husband’s has decreased. It’s not a huge amount like last time, but it would seem certain patterns are not always easy to erase. 2018 will be our year for paying down this debt, again, and hopefully we’ll have better control over our spending. Using Banktivity will definitely help us to see again where those missing dollars end up.

Great work John. I actually teach a course that recommends the “debt snowball” method and it works every time it is “used.” There are two rules to be adhered to with the debt snowball. The first is to stop digging the hole that placed you in debt. In other words, “quit taking out debt.” The second is to actually execute the plan. Many people list out their debts but, because it looks overwhelming,” they never start the plan and set up the actions to accomplish the desired results. Keep up the good work John.

I was really interested to read this article, but I think you buried the lead. The item that really helped you get out of debt so quickly was moving your credit card debt consolidated to a zero interest card. That saved you a lot of interest because usually credit cards have the highest rate of interest and should be the first item that you pay off with your debt snowball.

Probably a better option (some cards allow this) was to transfer your car loan to your zero interest credit card as well, to save even more money on interest and then make payments to just one consolidated loan.

Another option to consider is to get a consolidated line of credit – usually secured against your house – as they usually offer the lowest rates, other than integrating the loan into your mortgage.

Don’t forget trying to renegotiate your mortgage too – call up a mortgage broker and see if they can get you a better rate, even saving 1% on a 400K mortgage will save you around $27K on a 5 year term. There are a lot more options to optimize your mortage as well, without having to pay any extra (weekly payments, etc).

Thanks for the reply Kamal. Those are some good tips.